A motor accident compensation claim NSW residents need to understand can feel overwhelming, especially in the immediate aftermath of a crash. You may be dealing with injuries, lost income, and mounting medical bills, all while trying to figure out what you are entitled to and who to contact. The NSW CTP scheme provides real, practical support, but only if you act promptly and follow the right steps. This guide walks you through everything: who can claim, what is covered, how to lodge your claim, and what to do if things go wrong.

Table of Contents

- Key takeaways

- What a motor accident compensation claim in NSW covers

- Preparing to lodge: documents, deadlines and finding the insurer

- How to lodge your motor accident claim in NSW

- Avoiding common mistakes and handling denials

- What compensation you can expect

- My perspective on NSW motor accident claims

- How GKE Lawyers can help with your claim

- FAQ

Key takeaways

| Point | Details |

|---|---|

| CTP covers injuries, not property | The scheme pays for treatment, income support, and pain and suffering, not vehicle repairs. |

| Fault does not bar your claim | You can still claim even if you were partly at fault for the accident. |

| Lodge within 28 days | Lodging promptly protects your entitlement to weekly income payments and other benefits. |

| Liability decisions take about 4 weeks | Treatment costs are often covered during the assessment period to avoid delays in your care. |

| Disputes have a clear pathway | You can request an internal review within 28 days of a declined claim before escalating further. |

What a motor accident compensation claim in NSW covers

Before you lodge anything, you need to understand exactly what the NSW Compulsory Third Party scheme pays for, and who qualifies. Getting this wrong is one of the most common reasons people either delay their claim or abandon it altogether.

The CTP scheme is funded by the green slip insurance every registered vehicle owner pays. When an accident happens, the scheme provides financial support to people injured in that accident. Critically, CTP does not cover vehicle damage or property losses. That is handled separately through comprehensive vehicle insurance. The CTP focus is entirely on injured people and their recovery.

Who can make a claim

A wide cross-section of road users can access the NSW CTP scheme. This includes:

- Drivers injured in a collision with another vehicle

- Passengers in any vehicle involved in the accident

- Pedestrians struck by a vehicle

- Cyclists hit by a motor vehicle

- Motorcycle riders injured in accidents

One of the most important things to understand is that contributory negligence may reduce your compensation, but it does not eliminate your entitlement. You can still access treatment and income support even if you were partially responsible for what happened. This is a significant departure from the “all or nothing” thinking many people incorrectly assume applies.

What benefits you can receive

The CTP scheme covers a range of supports designed to help you recover and manage the financial impact of your injuries. These include treatment and rehabilitation expenses, weekly payments to replace lost income, attendant care costs, and lump sum compensation for pain and suffering (available to those with more serious injuries).

Pro Tip: If you are unsure whether your injury is serious enough to qualify for a lump sum payment, speak with a personal injury lawyer before making any assumptions. Many people are entitled to more than they realise.

Preparing to lodge: documents, deadlines and finding the insurer

Good preparation separates a smooth claim from a stressful one. Most delays and complications come down to missing information or late lodgement, both of which are entirely preventable.

What you need to gather

Before you lodge your claim, collect the following:

- Full details of the accident including date, time, and location

- The registration number of the at-fault vehicle

- Contact details of witnesses where possible

- Medical records and certificates confirming your injuries

- Proof of your pre-accident income (pay slips, tax returns, or business records)

- Photographs of the accident scene, vehicles, and your injuries

The more evidence you have from the outset, the stronger your claim will be. Do not wait for everything to be perfect before you start. You can continue gathering evidence after you lodge.

Time limits you must know

| Stage | Time limit | Consequence of missing it |

|---|---|---|

| Lodge initial claim | Within 28 days recommended | Delay limits weekly payments and available supports |

| Request internal review | Within 28 days of decline | Lose right to easy internal reassessment |

| Commence court proceedings | Generally 3 years from accident | Claim may be statute-barred |

Acting within 28 days is not just good practice. It is the threshold that protects your entitlement to ongoing income support from the moment your claim is lodged.

Finding the right CTP insurer

You need to lodge your claim with the CTP insurer of the at-fault vehicle, not your own insurer. In NSW, you can identify the insurer using the vehicle registration number through the SIRA website or by calling SIRA directly on 1300 137 131. Do not guess or assume. Lodging with the wrong insurer wastes time and may affect your entitlements.

Pro Tip: Take a photo of the at-fault vehicle’s number plate immediately after the accident. This single step removes the most common obstacle people face when trying to start their claim.

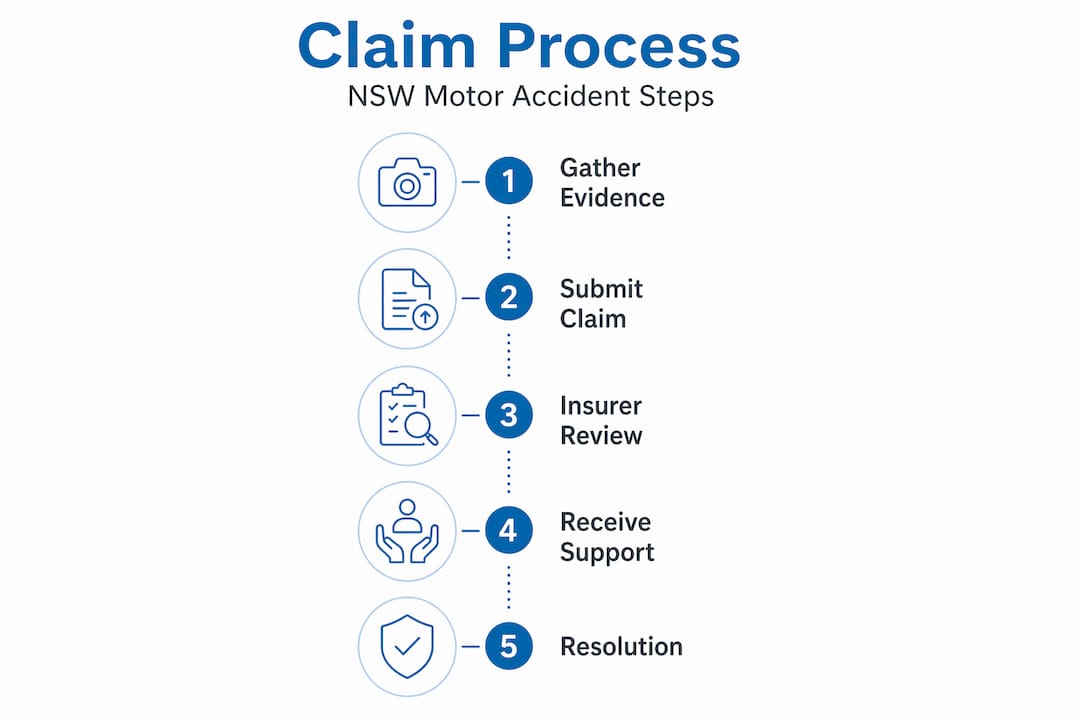

How to lodge your motor accident claim in NSW

Once you have your documents and have identified the insurer, you are ready to lodge. The motor accident claim process NSW claimants follow has two main pathways.

Your lodgement options

- Online via MyServiceNSW — The NSW government portal allows you to complete and submit the Personal Injury Claim form digitally. This is the fastest option.

- Directly with the CTP insurer — You can contact the insurer directly and lodge by phone, email, or post using the Personal Injury Claim form.

Both methods require you to complete the same form. The online pathway is generally more efficient because it creates a digital trail and confirms receipt in real time.

What happens after you lodge

The process following lodgement follows a clear sequence:

- The insurer acknowledges receipt within 3 business days of receiving your claim.

- A liability decision is made. This is the insurer’s formal acceptance or denial of your claim.

- A liability decision takes approximately 4 weeks after lodgement, though treatment costs related to your accident are typically covered during this period.

- Once liability is accepted, you begin receiving approved benefits.

- If the insurer requests additional information, respond promptly to avoid delays.

Comparing lodgement options

| Method | Speed | Paper trail | Best for |

|---|---|---|---|

| MyServiceNSW online portal | Fast | Automatic digital record | Most claimants |

| Direct to insurer (phone/email/post) | Variable | Requires your own record-keeping | Those needing guidance through the process |

Pro Tip: Keep copies of every document you submit and every communication you receive. Date and label each item. If a dispute arises later, your records will matter enormously.

Avoiding common mistakes and handling denials

Even well-prepared claimants sometimes run into problems. Understanding where things go wrong puts you in a far better position to handle setbacks confidently.

The most frequent errors in car accident claims NSW claimants make include:

- Incomplete claim forms — Missing fields or unsigned forms cause immediate delays. Review the form carefully before submitting.

- Late medical evidence — Failing to see a doctor promptly after the accident creates gaps in your medical record that insurers will scrutinise.

- Not disclosing pre-existing conditions — Failing to disclose relevant medical history can be treated as non-disclosure and may affect your claim’s credibility.

- Accepting early settlement offers without legal advice — Some initial offers significantly undervalue long-term treatment needs and income losses.

- Assuming a denial is final — A declined claim is not the end of the road.

If your claim is declined, you have the right to request an internal review within 28 days. This asks the insurer to reassess its decision. Many disputes are resolved at this stage without formal proceedings. You can find practical information on resolving disputes without court to understand your options before escalating.

If internal review does not resolve your matter, the Personal Injury Commission provides independent assessment and dispute resolution. SIRA also has oversight functions and can provide guidance when claimants face procedural barriers. Getting NSW accident legal advice early in this process is strongly recommended.

What compensation you can expect

Understanding the realistic outcomes of a claim helps you plan and make informed decisions throughout the process.

Types of compensation available

| Compensation type | Description | Notes |

|---|---|---|

| Treatment expenses | Medical, rehabilitation, and related costs | Covered from lodgement, including during liability assessment |

| Weekly income payments | Replaces lost earnings during recovery | Available if lodged within recommended timeframes |

| Lump sum for pain and suffering | One-off payment for non-economic loss | Only available for injuries meeting the serious injury threshold |

| Future loss of earning capacity | Compensates for reduced long-term income | Assessed based on your age, occupation, and injury severity |

Resolution timeframes vary considerably depending on the complexity of your injuries and whether liability is disputed. Straightforward claims where liability is accepted may resolve within a few months. Claims involving serious injuries or disputes over fault can take considerably longer.

Recent developments are worth noting here. SIRA’s two-year roadmap to improve insurer and health provider engagement aims to make treatment approvals more consistent and predictable. The focus is on clearer roles, better regulatory design, and improved education across the scheme. For claimants, this means more consistent engagement between health providers and insurers, which should reduce delays in getting treatment approved. These changes are being implemented progressively through 2026 and beyond.

Keep detailed records throughout your claim. Every medical appointment, every communication with the insurer, every expense incurred. This documentation directly supports your compensation outcome.

My perspective on NSW motor accident claims

I have worked with clients navigating motor vehicle injury compensation for many years, and the same pattern comes up repeatedly. People wait too long to act, and that hesitation costs them.

The 28-day threshold is not arbitrary. It exists because the system is designed to support people who engage with it promptly. In my experience, the clients who receive the best outcomes are not necessarily those with the most serious injuries. They are the ones who contacted a car accident lawyer early, documented everything carefully, and did not try to negotiate with the insurer alone.

I also want to address a misconception I see consistently. Many people believe that if they were partly at fault, they have no claim worth pursuing. This is simply not correct under NSW law. The scheme is genuinely designed to support injured people’s recovery, and partial fault is a matter of degree, not disqualification.

The SIRA reforms currently underway are, in my view, a genuine improvement. Greater consistency in treatment approvals will reduce the back-and-forth that so often delays care and frustrates claimants. The direction the system is heading in 2026 is a positive one. But the system still requires claimants to advocate for themselves and understand their rights. You cannot rely on the insurer to explain your full entitlements to you. That is not their role. It is yours.

Seek tailored legal advice early. Not because the process is impossible to navigate alone, but because the stakes are too high to leave anything to chance.

— Gaurav

How GKE Lawyers can help with your claim

Dealing with the aftermath of a road accident is stressful enough without trying to navigate a complex claims process on your own. GKE Lawyers has extensive experience handling motor vehicle accident claims across NSW, from straightforward lodgements to disputed liability matters. We offer clear initial advice, assist with gathering evidence and completing paperwork, and represent clients in insurer negotiations and formal dispute processes. Our team understands how the CTP scheme works and what it takes to protect your entitlements from the outset. If you have been injured in a road accident, contact GKE Lawyers today to discuss your situation and understand your options before time limits affect your claim.

FAQ

What is a motor accident compensation claim in NSW?

A motor accident compensation claim in NSW is a formal claim made under the Compulsory Third Party insurance scheme to recover costs related to injuries sustained in a road accident, including medical expenses, lost income, and pain and suffering compensation.

How long do I have to lodge a CTP claim in NSW?

You should lodge within 28 days of the accident to protect your entitlement to weekly income payments. Longer limitation periods apply for commencing legal proceedings, but early lodgement is strongly recommended.

Can I claim if I was partly at fault for the accident?

Yes. Contributory negligence may reduce the amount you receive, but it does not eliminate your entitlement to treatment costs and income support under the NSW CTP scheme.

How long does it take to get a decision on my claim?

A liability decision typically takes approximately four weeks after lodgement. During that period, treatment costs related to your accident are generally covered so your care is not interrupted while the assessment is underway.

What can I do if my CTP claim is declined?

You can request an internal review within 28 days of the insurer’s decision. If the review does not resolve the matter, you can escalate to the Personal Injury Commission for independent assessment and dispute resolution.